0% found this document useful (0 votes)

14K viewsFTC Takes Action To Stop Credit Karma From Tricking Consumers With Allegedly False "Pre-Approved" Credit Offers

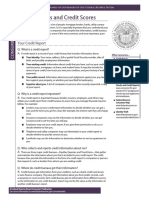

The FTC alleges that the company used claims that consumers were “pre-approved” and had “90% odds” to entice them to apply for offers that, in many instances, they ultimately did not qualify for.

Uploaded by

Mary Claire PattonCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

14K viewsFTC Takes Action To Stop Credit Karma From Tricking Consumers With Allegedly False "Pre-Approved" Credit Offers

The FTC alleges that the company used claims that consumers were “pre-approved” and had “90% odds” to entice them to apply for offers that, in many instances, they ultimately did not qualify for.

Uploaded by

Mary Claire PattonCopyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

/ 5