Another consolidation this year: Dialog is buying Atmel, although Atmel is fairly small compared to the other big players in the microcontroller market.

This sucks for consumers. Prices are already way to high for HDs and don't seem to come down anymore. It is as if there is some sort of price fixing going on.

I last bought some high capacity drives in 2011 just before the floods in Thailand zapped the industry, and I now note I can buy twice the capacity, 2TB -> 4TB, for $35 less.

There could be demand issues, as companies like Amazon, Google, Backblaze, etc. etc. buy them in mass quantities to offer redundant cloud storage.

At the other end, SSDs have got to be eating the lunch of small-moderate capacity SAS enterprise drives, and if not now, soon enough the basic sub 1 TB drives that workstations and laptops come with. I'm very conservative with these sorts of things so I avoided jumping on the SSD bandwagon, but a recent failure of one of my Seagate 15K system disks prompted me to buy one of Intel's lowest end, lowest capacity datacenter SSDs (DC S3510 80GB) and I don't think I'm going to be looking back....

What we see is that when we look at cost per MB ratio (price/MB) then it tends to go down exponentially. This happened from the beginning till 1975 when something happened so that the prices rose even above the initial levels in 1956.

But then it goes back down exponentially and it flattens around 1985. When we zoom in then we see that it continues to go down and then flattens around 1995.

The fall now accelerates as the ratio flattens already in 5 years.

Now when we move forward into into 2010, we see then continuation of the fall till sudden spike in 2012 when the ratio raises back to 2010 levels and then continues to fall and reaches the pre 2012 levels in 2014.

After 2014 the ratio still continues to fall.

Edit: So in cost per MB, we start with tens of thousands of $ per MB and reach tens of $ per MB in 1985.

Then reach tens of cents per MB in 1995 and in 2010 we have tents of cent per MB.

1TB WD Green EARS HDDs in 2010 for $70.

2TB WD Red HDDs in spring 2014 for $89.

1TB WD Black HDDs in fall 2014 for $90.

Just spot checked the same drives...

1TB WD Green EARS HDDs go for $57.

2TB WD Red HDDs go for $89.

1TB WD Black HDDs go for $71.

So prices are slowly falling but I don't think that we're going to see the rapid falls we were accustom to in the last decade due either to technological constrains or consumer demand, likely both.

From 2000-2005 we went from 20GB to 500GB drives, a 25x growth in 5 years but in 2010 we only had 2TB drives which is just a 4x growth. It's 2015 the largest consumer HDDs you can get from WD, Seagate, and HGST are 6TB, 8TB, and 10GB respectively. That's 3-5x growth for the 5 year period. Why has growth slowed? Is it a technological constraint or a lack of investment?

In the early 2000s you could only play music and movies you possessed so there was a big demand for storage space for all your ripped CDs and DVDs. In 2007 Netflix introduced online streaming and today we have thousands of choices for streaming video or music on demand which combined with cloud storage options negated our need for high capacity drives. I think the fact that people are opting for 120GB SSDs over 4TB HDDs demonstrates that the consumer need for extremely large hard drives is in decline.

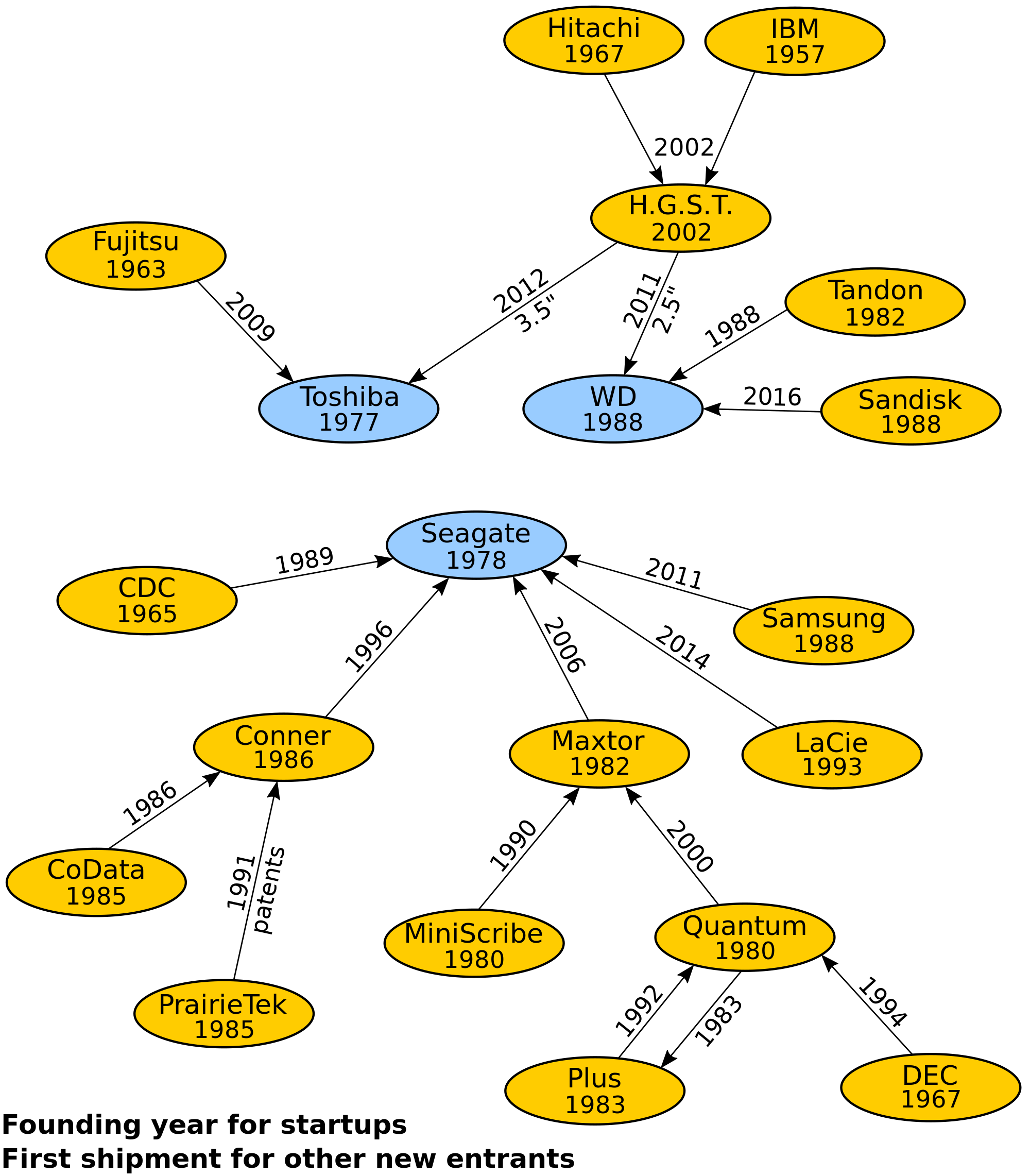

In the past the HDD makers were very competitive but if you look at WD, Seagate and HGST today you can see they're no longer competing on drive capacities. HGST is the only one that even bothers to sell a consumer grade 10TB HDD. Western Digital has been diversifying for years; first it was portable backup solutions, then NAS drives, NAS solutions, Surveillance and Data Center drives, and just today they announced they're buying Sandisk, a major SSD player.

I think the industry as a whole is moving away from HDDs and for that reason they nolonger need to compete so ferociously on price points.

Quibble or more about your useful exposition, especially WRT:

That's 3-5x growth for the 5 year period. Why has growth slowed? Is it a technological constraint or a lack of investment?

Could be technological. A few years ago I read that magnetic hard disk areal densities were doubling roughly once a year. However, unlike the process node shrinks that allow Moore's law, don't disk improvements come from either small incremental things or huge improvements like giant magnetoresistance (GMR) heads? So the companies could have, for the time being at least, run out big technological advances.

In fact, while I'm not following this at all closely (for various reasons I'm planning on keeping a 4 TB cap on my home storage), the biggest new thing I've read about is shingled recording (https://en.wikipedia.org/wiki/Shingled_magnetic_recording), where writes are partially overlapped, and rewrites are expensive. Per that Wikipedia article, this can add 25% to the capacity of a drive ... which in the context of a previous doubling per year isn't much, it's more of a small incremental improvement.

The other side is demand, of course. I'm not sure on general principles that consumer demand for big drives is down that much, for a small SSD for active stuff + a big nearline drive for media makes a lot of sense. Especially if your Internet connection is capped like mine. This is the approach I've taken since 2007 (with heavy use of high quality CD-Rs for the 2000-2006 period).

Another factor might be an accumulation of people losing too much data on their big hard disks.

Finally, I have to wonder if the big cloud storage providers are slowing down big capacity disk purchases. That'll in part depend on how they use them, do they split out disk farms from compute, or use more homogeneous approaches, such as "moderate" sized disks attached to most machines?

I think technologically we've come to an impasse for the reasons you've pointed out, but I suspect that the average user also has little demand for drives greater than 1 TB in capacity which might be just as big a factor. I'm not saying that an individual's combined storage requirements don't exceed that but rather than no one storage need requires drives with a greater capacity.

HGST 8TB is keeping its high price for about a year already. Prior to that they had wonderful 4TB drives for ~$100 for home NAS, the price for 8TB version is like 6x higher and their 4TB drives are no more since WD acquired them (and Seagate's 8TB home drives have poor reliability, HGST being the only reliable HDD manufacturer atm). Seems like we are in a sort of a limbo when there aren't any reasonably priced SSDs >1TB and HDDs are stuck at 8-10TB for a while already.

As for SSDs, most of the optimization goes to improving bandwidth (where most people won't notice a real-world difference between an SSD plugged into SATA2 and M.2 PCIe baring 8k/4k video creation), but anyone will notice a real-world difference in increased IOPS, which no company cares about and they plateaued at ~100k IOPS for the past few years (i.e. some of the low-end Sandisk SSDs with 4k IOPS are subjectively as slow as HDDs).

Physical disks are not going down in price because their market volume is shrinking, their technology is just not evolving. On consumer machines, the 5400rpm drives are being replaced by other 5400 or by SSDs, not by 7200rpm. So the 5400 disks don't go down in price, whereas SSDs do (albeit slowly, due to technological constraints).

I'd say SSDs are going down in price pretty dang fast. The technology is advancing far more rapidly than HDDs could ever dream of. The Samsung 850 EVO 500GB is already ~25% cheaper than the equivalent 840 was a year ago, with better performance. Not to mention the high performance NVMe drives we're starting to see, where the price:performance is even better.

i think the main parameter people judge price reductions for disks is "$ per GB", rather than anything related to performance. SSDs are getting better and faster, but the price per GB is not exactly crashing.

Really. Seagate enterprise highest duty cycle "nearline" drives, 5 year warranty (which I not long ago had to use for one of the 2 I bought back then).

A SAS interface adds $20 currently; models and Newegg prices:

Constellation ES ST32000444SS 2TB $265 7/15/11 SAS

Constellation ES.3 ST4000NM0023 4TB $230 10/21/15 SAS

Constellation ES.3 ST4000NM0033 4TB $210 10/21/15 SATA

ADDED: Samsung magnetic hard drives are going to be bad for historic price comparisons, for Seagate bought their unit in 2011 (http://www.seagate.com/about-seagate/news/seagate-completes-...). Per that press release, "To ease the transition of products and technologies, Seagate will retain certain Samsung HDD products under the Samsung brand name for 12 months";

Your old price might be lower than normal due to that sale, and/or whatever prompted Samsung to get out of the business; the current price is close out inventory of older generation technology.

A 1TB spinning-rust disk is quickly becoming a niche product. Looking quickly on Amazon, a 1TB drive is ~$50 while you can get a 5TB for ~$150. The price has plummeted, just not at that capacity.

Prices of hard drives historically haven't come down. For a very long time consumer hard drives have been between $50 to $200. What changed over time was the size of the drive you could get for $X.

That's still happening, but it's happening a lot slower than it used to be.

That's an important point. Drives the same size as those 5 years ago go down in price, but at some diminishing rate as they asymptotically approach zero $.

With storage its hard to say exactly what its doing, because it won't hold still to be measured. You have to allow multiple variables to change in any stats collected over time (capacity, physical size, speed, volatility).

It seems reasonable to chart the price of some standard capacity (most common?) over time. Is that changing any more?

You can buy a Seagate 5tb external for $136 on Amazon.

I was paying that much for 1tb to 1.5tb just a few years ago. That's a significant improvement. Prices have fallen by half for 1tb (~$50); and at the $125-$135 price point, capacity has increased by ~200%.

I fail to see how prices are way too high. Current prices are a steal in my opinion.

SandDisk SSD's aren't cheaper, not when you are comparing oranges to oranges, they sell allot of very very low end SSD's their performance series costs more than comparable drives from Samsung.

There are other companies that also sell cheap SSD's like Micron and Crucial but the big names Samsung, Intel, OCZ(Toshiba) usually sell quite high end devices.

Samsung pretty much blew the market out of the water with their Evo series it comes very close to the performance of it's Pro series and other high end SSD's out there where it comes to real world use at a fraction of the cost. It brought the costs of SSD's down to less than 350$ per TB while keeping outstanding performance and life span.

I don't think WD has any motivation to increase prices. The point isn't to stop SanDisk from competing with them. They need a SSD product and acquisition is easier for them than developing their own.

What I wonder is if WD will continue the green and blue lines. The writing is on the wall for spinning disks. They may reduce the number of HDD models they sell and make SSDs the new green.

They probably won't. SanDisk already make the most expensive flash drives, as well as cheaper consumer models. But I have a couple of their top shelf drives, like the "Extreme Pro" USB3 stick. They're stupid fast, and worth every penny, assuming it has a long life.

I don't think I've seen them ever come down within the past 10 years, all that happens is that storage space goes up and smaller drives stop being produced.

I always have thought that companies were bought for a price of it's market value (stock price * number of stocks), or if someone did not wanted pay all in cash they would've tried to compensate in other ways until market value is reached.

But here WD bought SD for ~85-86$ per share, when it was worth ~75$ per share. It's at least 13% more.

Does it simply mean that WD hopes that SD will rise in value rapidly? Or I imagined company buying evaluation wrong?

If WD were to start buying sandisk share-by-share, then the price would go up. By the time they owned 50+% their average share price would be a lot more than $86.

Owning 100% of sandisk is more than 100 times as valuable as owning 1%. With 100%, WD can tell sandisk what to do, has access to their IP, can merge steps in the production process, etc.

You can still do that with majority ownership (e.g. 51% of shares). The difference with owning 100% is that you have to share dividends with the other 49%, which makes it difficult to move money out of a company.

This is a common misconception by non financial people (no offense). You have to look at this from a finance and risk perspective.

1. Cash lying around in your bank account is usually a poor use of working capital (you are effectively "losing" money by it sitting in the form of cash)

2. Investing in "innovation" is always risky. Look at how many internal Google apps get scrapped a year or two into launch. They effectively write those off and it's a direct loss to Google's bottom line.

3. "Innovator's Dilemma" - big companies realize they are not the best suited to invest in innovation, hence why startups and buying them are actually a net positive for large businesses.

Bit first, this is not cash lying around, this is new debt. Second ,Even if you take all of Google's investments into innovation and and look at them combined ,they would probably offer a decent return on investment. Similarly if you look at intel capital's investments , you'll probably get a nice financial story + a decent strategic lever.

Also from a pure financial perspective - sandisk has a profit of $1.22 Billion.That would take 15 years to repay. Isn't risky to make such long term investments in i a single investment , in tech , which is a dynamic field usually ?

1. This is not cash in a bank.

2. Innovation is a requirement not an option.

3. Innovator's Dilemma completely contradicts the point you attempt to make in #2.

Considering they are only over paying by roughly 10% if you assume the current stock price is fair then they are "only" throwing away $1.9 billion. They probably can't develop their own flash technology and build a fab for that amount of investment.

To make some sort of (of course flawed) comparison:

You want a nice house.

You can drive around the neighborhood, look at what houses exist and inspect the house you are interested in from roof to cellar bevor making an offer. You adjust your price for the parts you think need renovating, market conditions etc. Banks will gladly finance the deal, you don't need to have very much money of your own.

Or you buy an empty plot, buy a lot of materials, hire people to turn the materials into a house of your specifications. In many established neighborhoods it's very hard to even get an empty plot. Maybe you don't find the materials or people in the quantity or quality you want. Maybe your plans are not that good. Maybe the weather is bad and you take much longer than you planned, and you can't stop at half a house when you run out of money. If everything goes well you can get a better house for less money, but you have to be able to afford the risk.

There are two main ways to buy a public company. One way is to make a deal with the board of directors which gets ratified by the shareholders in a vote. Because stocks are highly liquid you really have to offer a premium over the current stock price for that to be a good deal for everyone involved. Then think about what happens after the board agrees to the sale, people can still trade their stocks on the open market, but it'll be a vastly different landscape than normal because those stocks now have a fixed price at a future date. So it doesn't make sense to buy stocks at higher than that price, it also doesn't make much sense to sell stocks at lower than that price unless you need liquidity now.

The other way is to just buy up a majority of the public, voting shares, typically called a hostile takeover. This is the hard way, and can become extremely expensive if enough people decide they don't want to part with their shares except at very high prices. As you buy up shares the price will go up, so it ends up being a longer, more difficult, less certain, and more contentious way to buy a company.

In theory, owning a controlling stake in the company is worth something beyond the price of an individual share, because it gives you the power to affect the outcome of the business. The difference between acquisition price and current market value is often referred to as a "control premium" and 13% isn't a particularly big one.

That depends on who issued the debt and what happened after that. If WD issued the debt, they could use that incoming cash to pay the old stockholders to gain the shares in SanDisk. That would be a real cash outflow. Bigger company after the transaction, and bigger debt.

Alternative is that WD pays cash to stockholders they might have had lying around. Then issue debt in SanDisk and pay dividend upstream from Sandisk to WD afterwards. Bigger company, and bigger debt result, only different place for the debt. Sometimes tax incentives help which route to choose (private equity often loads up firms on debts, since interest is deductible).

Only way to 'pay less' would be (happens sometimes) that you can buy a company that holds a lot of cash, but that has a relatively low valuation one way or the other. Perhaps stockholders sense risks and don't expect dividends (market cap in that sense is expected value of future earnings plus lots of noise). Then you buy company, and use the cash for superdividend right away. Bigger company results, but with relatively stronger solvency since you've paid part from cash that was 'undervalued'.

{kind=link}

1. Intel-Altera: http://www.bloomberg.com/news/articles/2015-06-01/intel-buys...

2. Avago-Broadcom (and earlier, Avago + LSI): http://www.bloomberg.com/news/articles/2015-05-27/avago-said...

3. Silicon Imaging-Lattice: http://www.wsj.com/articles/lattice-to-buy-silicon-image-for...

4. NXP-Freescale: http://www.eetimes.com/document.asp?doc_id=1327236

5. (2014) Cirrus-Wolfson: http://www.eetimes.com/document.asp?doc_id=1322171

6. Avago is further looking at Xilinx, Maxim, and Renesas: http://www.reuters.com/article/2015/05/14/us-chipmakers-m-a-...

This is one industry that is in flux ATM.

Edit: Further afield, though tightly coupled with this industry, on the manufacturing equipment side, Lam Research announced acquisition of KLA-Tencor today http://www.wsj.com/articles/semiconductor-firm-lam-research-...