Then switch from these services while they are still only a few. Revenue is a language they understand. I never understood why anyone would even want a banking app though; there is nothing int can do that a website can't.

The browser war can at least still be won or settled; mainstream apps are a lost cause outside the legal arena.

Edit: and by switching i don't mean going to some tinfoil grayweb nonsense. Go to their direct competitor.

I think the problem with the revenue rhetoric is that these services are consumed by the general consumer and the people that read this discussion generally are only a neglibile size of that market segment. So, even if all HN readers affected and all wired reader, etc changed service due to this discussionit would still be a rounding error on that company's report sheet in the end.

> I never understood why anyone would even want a banking app though; there is nothing int can do that a website can't.

Some banks are phasing out code cards or SMS verification for 2FA, and the only way to get the second factor for logging into the online banking website on your computer, is to use the bank’s app on your phone.

Obviously other solutions could be implemented if the bank chose. But if the bank does not choose to implement those other options, and instead requires the use of their app, then that explains for the OP’s sake some of the interest in running the bank’s app instead of solely using the website.

Ditto. I must have spent 10 full minutes clicking all through my bank's website before I finally realized their phone app provided the only possible way I could make a Zelle transfer.

My HOA started mandating Zelle as the only way they will accept payments. So now it appears that I have no choice but to use a device that supports my bank's app if I want to avoid getting a lien put on my house.

> Does it not count as a debt, that they have to accept cash ("legal tender for all debts public and private") for?

Let me tell you how that tends to go down in the real world. The HOA doesn't have a physical office or anything. It's some random address and random suite. Maybe it's a document processing company or some other third-party processor. There's some non-trivial chance that some $15/hr kid who may or may not have been raised right is opening the envelopes and feeding the contents into a scanner.

So I stuff my HOA dues in cash in an envelope and then go down to the post office to stand in line and get it delivered certified with a return receipt. I get the return receipt. Then the HOA puts a lien on my house. I say, "But I made the payment on time!" Then they say, "Naw-uh." Then I say, "Sure I did, I sent it in cash and I have a return receipt." They say, "We have no idea what you're talking about."

<sad trombone>

> Or there should be the option of opening another account, at a less tyrannical institution, to use for those payments.

How can I find out which ones let me use Zelle through their website? I don't trust anyone I can find at a branch or on the phone to give me the correct answer, because chances are they all personally use the phone app and really have no idea. I guess I can start opening up random accounts with random banks until I find one that works. For now.

I think we're missing the point entirely by talking about cash and hopping around banks and all that. The point many people are trying to make here is that life is already being made unreasonably difficult for those of us choosing to use Libre computing platforms, and there's a plausible reality in the future where choices go from inconvenient to scant to nonexistent.

I did, i use firefox for example, but with mobile phones, what's the alternative? Apple and its walled garden? And when filing my taxes only works via chrome, how do i switch countries easily? Move because of a browser limitation and leave everything behind?

Not that it is for everyone; but i have used Sailfish OS for just about 10 years, and it has been quite fine.

Any country that isn't a total sh*tshow will have accessibility regulations around that. Let the accessibility folks fight for you.

That same logic says you should not vote either.

If even some 10-20% of IT professionals (with salaries to match) up and leave for a less shit bank, trust me, they will care.

You assume there is a “less shit bank”. Not everywhere is like the USA with a wide choice of banks. In some countries the banking landscape has, through mergers, become limited to just a few choices, and they all require SafetyNet attestation for their phone apps.

"voting makes no difference" is one of those rules which apply really well to the individual, but if you apply them to a larger group of people, they become wrong.

You would be trading one kind of "shit" for a much more real and serious kind of shit - at the new bank, you'd either be more likely to get your account drained in ways that are hard to reverse, or you'd be forced back to using dedicated hardware smartcard readers of the type that were common before mobile apps became widely used (at least were common in Europe).

If your bank account gets drained and you'd made a big song and dance about how you selected that bank specifically because it had less security on its mobile app, well, nobody will have any sympathy for you.

If your bank is equally secure but uses dedicated hardware devices instead of smartcard readers, then all you did is swap one bit of secured hardware for another, making your life less convenient and in return for what?

A bank has to know it's communicating with the real human who owns the account and not a hacker. It's going to achieve that one way or another. You'd be much better off accepting the tech and finding ways to achieve your goals within it, like by setting up a project to maintain whitelists of known good/secure OS builds. You can then make libs that wrap SafetyNet and eliminate the false positives. Even if banks don't start using it anytime soon, other smaller companies might and it's a place to start. Of course the fact that virtually nobody cares about custom operating systems to begin with is the biggest hurdle you'd face, not the tech or business requirements, but that is partly on the OS developers. You can't complain nobody cares about if you're not giving anyone a reason to care.

You use the word “forced” like it’s a problem? I hated it when my bank got rid of a nice secure card reader (which required my physical card and pin).

If my phone breaks or is stolen, I can’t actually buy a replacement phone now, as that requires spending money, which requires 2FA which requires my phone.

> That same logic says you should not vote either.

Indeed.

> If even some 10-20% of IT professionals (with salaries to match) up and leave for a less shit bank, trust me, they will care.

That's an impossible number of people to coordinate on something like this, and even if, I doubt banks would care. There exist no less shit banks, and retail is a rounding error anyway.

Banks aren't shit because of incompetence or a not-give-a-damb attitude. They're shit because it makes them more money, both directly and by reducing risks.

>I never understood why anyone would even want a banking app though; there is nothing int can do that a website can't.

A mobile phone app can let users "deposit paper checks from home" without ever driving to the bank branch by taking a photo of the check with the smartphone camera. Last time I looked into it, a desktop website couldn't enable check deposits with a webcam. (EDIT: I don't mean technically not possible. I meant that the banks deliberately chose not to have the websites utilize desktop/laptop webcams as an alternative to smartphone apps.)

Smartphone bank apps also have "push notifications" to immediately alert you of suspicious activity on your account.

But if one never uses the extra features that smartphones bank apps enable, then yes, desktop bank websites can be seen as perfectly equivalent.

Meanwhile most of the world hasn't used checks in 20+ years. Thank god for that.

But for completeness; browsers have been able to use cameras since before smartphones. So of course it can work just the same there.

"Suspicious activity" is such a bad strawman argument, i'm not sure how to address it.

"Just thought you'd want to know your money is gone, lol."

Either you do N+1 factor authentication for real, or you just shouldn't bother.

Browsers have had push notifications for quite some time now too... so even if it was a worthwhile feature, it doesn't need an app.

>Meanwhile most of the world hasn't used checks in 20+ years.

True, but the key word you used is "most". E.g. My home insurance refunds an annual dividend back to me and their method to pay me is paper check. Not an electronic direct deposit, nor a VISA giftcard, nor even a "credit" that can be applied as a discount off year's premium. It's a paper check.

>So of course it _can_ work just the same there.

Sure but that's talking in hypotheticals. Today, I have the reality of a paper check to deal with and Bank of America and Chase websites do not have options to upload images of checks for deposit. (Chase does have a paper check scanner option that doesn't require mobile phones but that's only for commercial accounts: https://www.chase.com/business/banking/services/quick-deposi...)

>"Suspicious activity" is such a bad strawman argument, i'm not sure how to address it. "Just thought you'd want to know your money is gone, lol."

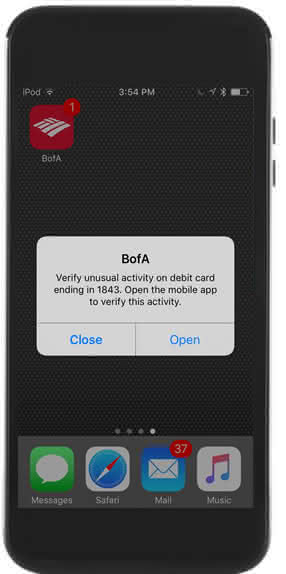

No, you misunderstand. The better banking smartphone apps will require interactive approval from you to allow a particular suspicious transaction to happen. This prevents your money from being gone. (Example screenshot: https://www2.bac-assets.com/online-banking/spa-assets/images...)

> Browsers have had push notifications for quite some time now too...

No, web push finally came to Safari in iOS 16.4 which was just a few months ago in April 2023.

From the tone of your reply, it seems like you'd rather be argumentative instead of acknowledging that bank apps have some extra features that's convenient for some users.

The paper check scanner from Chase also (last I looked) cost a few bucks and needs an app on the Windows PC to process the data. That hardware is only useful when you process 100s of checks (eg: grocery store).

The real use for notifications is to sell things or get paid for services in-person without cash. The notification provides certainty that you've been paid, so you can hand over the item/stop hanging around after the service waiting to be paid.

Of course, a bank should be able to send you a text on the service of your choice. But they won't.

? Suspicious activity isn't about this. For instance my bank reports me when I get a double debit (e.g. go to a restaurant and get charged twice), when a regular expense increases (e.g. some monthly payment that suddenly goes up)...

My credit union let me deposit checks via uploaded picture on browsers back around 2008ish. Don't get me wrong, I did this by taking a picture from my phone and emailing it to myself to upload - the smartphone UX simplifies that. But this is a trail long since blazed.

Yes, this is one of those things that banks will sell as an add-on because capitalism. Credit unions will either just not have their act together on it (i.e. they contract with a bad service provider) or will have all kinds of useful stuff like this for free.

I really want a general-membership credit union with stellar technology, but I haven't found one yet. Does your credit union by chance offer open membership?

If you're in the US, write to the FTC and complain that this is discriminatory toward the disabled who may need special user agent accessibility features unavailable in Chrome.

{kind=link}

Edit: and by switching i don't mean going to some tinfoil grayweb nonsense. Go to their direct competitor.