Go find a graph of housing prices 1963 to current, you will see that the events leading up to and including 2008 did nothing to help or hinder housing affordability in the long run. We are due a 2008 style correction but that will not make housing affordable either. The real problem is that household income stopped outpacing home prices in the 1970s.

The core actual problem is that there are good places to live, and finite land in those places.

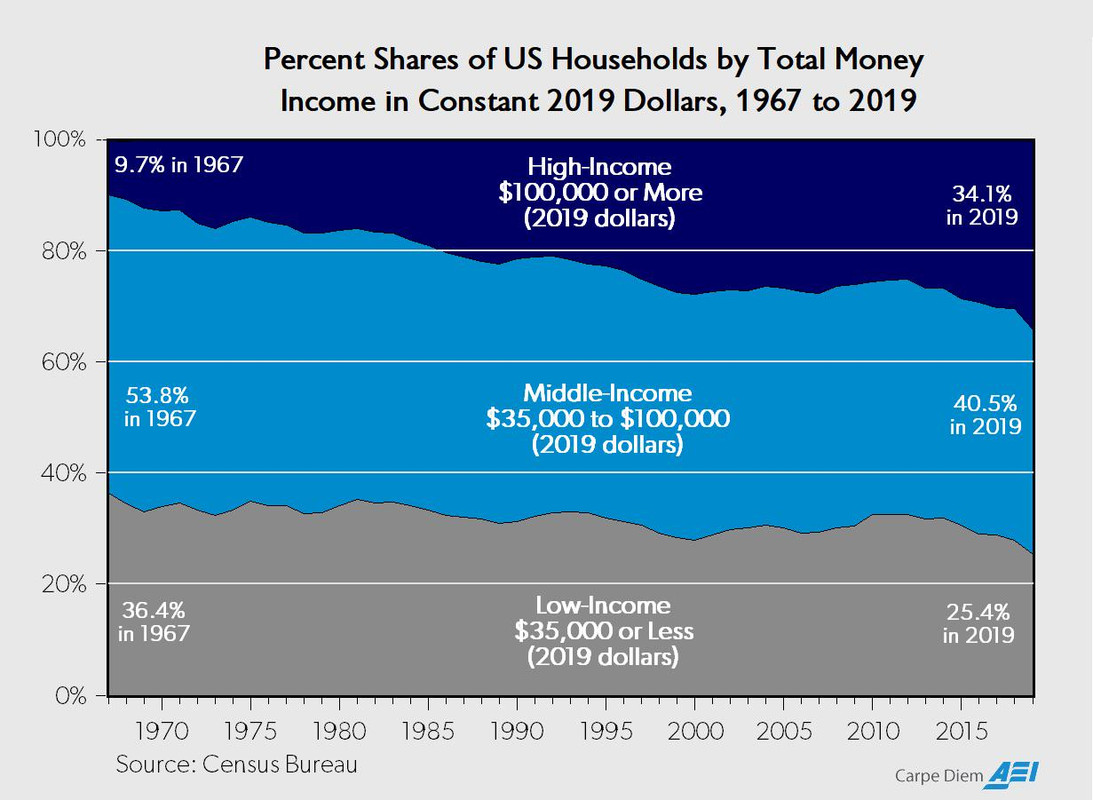

The next step up "problem" is that the income curve has flattened greatly in the last 75 years. So there are many more high earners mixed in that they are carrying "regular home" prices up with them.

In 1967 lower/middle/upper class ratio was 36%/54%/10%

In 2019 lower/middle/upper class ratio was 25%/41%/34%

The middle class is shrinking because people are getting richer, not poorer. That's the part you never hear people say. Probably because they don't even know it and just assume everyone is broke.

I can only imagine now, after the pandemic money shower (not stimulus checks), that this effect is even greater. Hell upper class might actually be at parity with middle class now.

No. It is thinking of and treating homes like an investment, and the lack of laws to discourage that. Housing prices have little to supply -vs- demand for actual housing, it is demand for housing as an investment instrument that drives prices. Do you think in 2008 suddenly fewer people needed places to live?

That chart says it’s for households, not individuals so for the time scale shown (70s onwards) all you’re seeing is that 1 earner households became 2 earner households.

The stuff about upper class growing does not follow from that. Poor analysis.

You can't just make new places attractive, they usually are proximal to valuable resources or land features. A dramatic example of this are the arab states that are trying to brute force make the desert an attractive place to be. Nothing in those cities is economically organic, it's all oil money trying to LARP functional cities built in logical locations.

> A dramatic example of this are the arab states that are trying to brute force make the desert an attractive place to be

They're doing it wrong. I'll point to places adjacent to the sahara building a "green wall" which is turning parts of the sahara back to a savannah and replenishes the water table.

I think you are confusing nature with economic vitality. There needs to be economic value inherent in a ___location for a city to thrive. Having grass and water doesn't mean much at all in this regard. You need things like natural harbors, navigable river ways or mine-able resources.

Pretty much all the good spots for cities have already been claimed, hundreds of years or even millennia ago. These are the spots people live in, and the spots people want to live in (as evidenced by ever increasing cost to live there).

> Having grass and water doesn't mean much at all in this regard. You need things like natural harbors, navigable river ways or mine-able resources.

Harbors? No. Trains and airplanes exist.

River ways? Los Angeles and California have demonstrated, with the LA river, that rivers can be constructed. Also, trains and airplanes exist. Wanna complain about no water? Well that's where land revitalization comes in.

Mine-able resources? Perhaps. There are lots (!) of resources in deserts that aren't mined. I also argue that food is basically a mine-able resource. I also argue that many resources can be imported instead. I also argue that plenty of people can work remotely without ever working a field or a mine.

In my state the people are there because there is water. You can't make new places attractive, because all the people will be dead. It's basically a 100% correlation between ___location of towns and whether you can economically drill or divert water there.

How are those class strata thresholds defined? I usually see it defined as quintiles, so by definition the distribution remains constant but the money to get there changes. I think upper/lower class are usually defined as the top/bottom 20%.

It's REITs that distort the market most. They can gobble up homes with insane price insensitivity and wait for their rental payoff in 30 years all while trading them around as derivatives.

In the locales where one has a decent chance of earning more than $100,000 (like the Bay Area) that income is significantly below poverty level, even as a household of one. That is definitely not "upper class" by any definition.

Put differently: this chart shows the average temperature of the patients in a hospital. You can't just show average income across all of the US without considering cost of living and pretend that this result means something.

> The real problem is that household income stopped outpacing home prices in the 1970s.

On a price per square foot basis, home prices have been remarkably stable since 1960s. The share of income spent on housing has also remained remarkably stable. Though prices have ballooned, interest drops considerably, so monthly payments as share of income haven't changed that much.

The way things have gotten worse for people isn't so obvious. For one thing, people have many more choices to spend their money on, such as computers and college. That's created additional pressure on people without the cost of housing itself changing as much as people think, but its a problem someone from 1960 might roll their eyes at. (Hedonistic adaptation?) Then of course there's various income and geographical bifurcations. For example, you can choose to live someplace cheap, but then you're opting out of the highly dynamic and potentially highly lucrative portions of the economy. That's an opportunity cost, but not a literal cost if you're comparing to 1960s lifestyles.

>The share of income spent on housing has also remained remarkably stable. Though prices have ballooned, interest drops considerably, so monthly payments as share of income haven't changed that much.

That is not a good thing for new buyers. It is fantastic for people who bought when prices were cheap and rates higher, because now they have a low mortgage and low rates (refinance). But new buyers must now find higher deposits and have no real hope of every paying their property off early because any over-payments make only small dents in the high prices.

>On a price per square foot basis, home prices have been remarkably stable since 1960s.

I’m not sure that’s true, in fact I’m quite sure it’s not, but I’m willing to change my mind if you have a good source. In particular, home sizes have shrunk since 00 and prices have surely not gone down so it could only be true prior to then if at all.

It depends on how far you want to go back for comparison. The average house size has grown a lot since the 1960s, but dropped some more recently since the housing crisis. But it’s still up, and by a pretty big margin. In the 1950s, the average house was < 1k sqft, today it’s pushing 2.5x that. It’s even larger when computed on a per-person basis.

If you don't trust the sources of those articles, note that I was skeptical, too (of similar articles I had read), which is why I went looking for primary sources.

There's a similar phenomenon with home ownership. The percentage of homeownership has only varied by a few percentage points over the past 60+ years. However, what has changed is the median age of homeowners: they tend to be older. In particular, younger people tend to wait longer to purchase a new home. Now, there's two ways to look at that: they wait longer because they need to spend more time saving money or they wait longer because they want to buy bigger homes or move into more exclusive neighborhoods. And those aren't mutually exclusive. But then there's also the demographic shift toward older Americans generally, which means younger people are competing with older people (with more savings) for homes.

The financial pressures are real, it's just that the sources of those pressures are much more complicated than in the popular discourse.

Last year I built a house for ~30k shell, about ~60k with utilities and everything inside of it. My own labor.

Of course, there are only a handful of counties that will let you do that without licenses, or a building plan, or inspections at times that preclude holding a job. Because there is always some self-righteous actor, screaming at the rooftop that their neighbor is going to kill the whole neighborhood in a fire, no matter that housing has been virtually completely unregulated for owner/builders in my county for 2 decades and none of the hysteria people warned of came to fruition.

The plus is all these people screaming for expensive regulations are absolutely scared shitless of my area, and do not live here. Which is nirvana.

That may just be regulatory inertia keeping you safe.

Most people aren't building insanely stupid and dangerous homes because in most places they legally can't, and very few work specifically just in your county, so they just do what they mostly do, which is mostly safe and up to code. Maybe they cut a few corners. Probably a few weirdos doing entirely their own thing.

By the same token, if your weird neck of the woods made seatbelts non mandatory, it wouldn't mean everyone takes them off as they drive through, so the subsequent maintained levels of vehicular loss of life would say nothing about the increase of safety seatbelts provide. A few weirdos might be taking the belt off, though!

Still, it'd only take one weirdo's entirely preventable and lethal to their kids house fire/car crash to prove them idiotic and probably get the law changed.

Many people and kids die from effects of homelessness yet regulations that make houses less accessible persist, so I'm not confident of your thesis people will fix the laws to save the kids.

I would posit one of the best things we could do to save children would be to completely deregulate the housing industry and eliminate trades licensing. This would not only enable housing accessibility but more money for education, healthcare, and good food for kids.

{kind=link}